Australian CGT Calculation

How PrivateACB calculates capital gains tax for Australian cryptocurrency using lot-based tracking (FIFO, LIFO, HIFO), including the 50% CGT discount for assets held over 12 months.

Overview

Section titled “Overview”The Australian Taxation Office (ATO) treats cryptocurrency as a Capital Gains Tax (CGT) asset — not as currency or foreign exchange. Every disposal of a crypto asset triggers a CGT event, most commonly CGT event A1 (Section 104-10, ITAA 1997). PrivateACB calculates your capital gain or loss for every disposal, applies the CGT discount where eligible, and generates the reports you need for your tax return.

Australia uses lot-based (parcel-based) tracking — the same fundamental approach as the United States. Each purchase of crypto creates a separate parcel with its own cost base and acquisition date. When you sell, PrivateACB matches the disposal against your parcels using your chosen method.

How It Differs from Canada and the US

Section titled “How It Differs from Canada and the US”| Feature | Canada | United States | Australia |

|---|---|---|---|

| Method | Average Cost (ACB) | Lot-based (FIFO/LIFO/HIFO) | Lot-based (FIFO/LIFO/HIFO) |

| Loss denial | Superficial loss (30-day window) | Wash sale (30-day window, optional) | None (Part IVA is intent-based) |

| Holding period benefit | None | Short-term vs long-term rates | 50% CGT discount (>12 months) |

| Per-account tracking | No | Yes (T.D. 10000, from 2025) | No |

| Tax year | January – December | January – December | July 1 – June 30 |

| Currency | CAD | USD | AUD (A$) |

Lot-Based Tracking (Parcel Method)

Section titled “Lot-Based Tracking (Parcel Method)”Every time you acquire cryptocurrency — through a purchase, a trade, staking rewards, mining, or an airdrop — PrivateACB creates a parcel (tax lot) recording:

- Acquisition date — when you acquired it

- Quantity — how much you acquired

- Cost base — what you paid, including transaction fees (the first element of the 5 cost base elements)

When you dispose of crypto, PrivateACB selects which parcels to use based on your chosen method:

FIFO (First In, First Out): The oldest parcels are used first. This is the most common method and the ATO’s default assumption.

LIFO (Last In, First Out): The newest parcels are used first. May result in more short-term gains.

HIFO (Highest In, First Out): The parcels with the highest cost base are used first. Minimises realised gains.

Worked Example (FIFO)

Section titled “Worked Example (FIFO)”| Date | Action | Quantity | Price (A$) | Parcel |

|---|---|---|---|---|

| 1 Jul 2023 | Buy 1.0 BTC | 1.0 | A$50,000 | Parcel 1 |

| 1 Oct 2024 | Buy 0.5 BTC | 0.5 | A$60,000 | Parcel 2 |

| 15 Jan 2025 | Sell 1.2 BTC | -1.2 | A$65,000 | Parcels 1 + 2 (FIFO) |

Using FIFO, the 1.2 BTC disposal is matched against:

- Parcel 1 (all 1.0 BTC): Gain = (1.0 x A$65,000) - A$50,000 = A$15,000 (held >12 months — CGT discount eligible)

- Parcel 2 (0.2 of 0.5 BTC): Gain = (0.2 x A$65,000) - (0.2 x A$60,000) = A$1,000 (held <12 months — no discount)

Total gain before discount: A$16,000 After 50% discount on Parcel 1: A$15,000 x 50% + A$1,000 = A$8,500 net capital gain

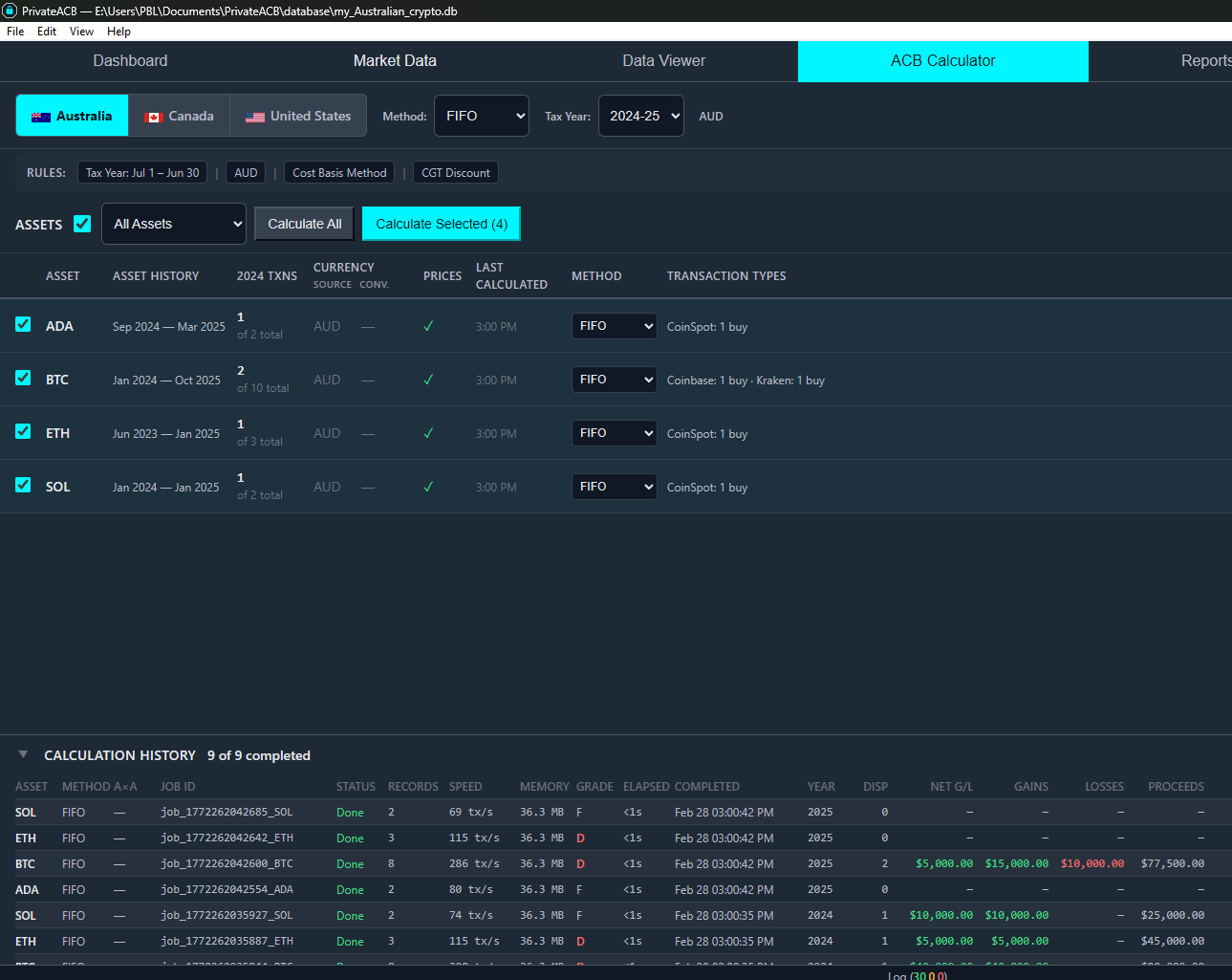

The 4-Zone Calculation Dashboard

Section titled “The 4-Zone Calculation Dashboard”PrivateACB organises the calculation workflow into four zones:

Zone A: Configuration Bar

Section titled “Zone A: Configuration Bar”At the top of the Calculation Dashboard, you will see:

- Jurisdiction toggle — Select “Australia” (shows the Australian flag)

- Tax year selector — Shows fiscal years in “2024-25” format (July 1, 2024 to June 30, 2025)

- Method selector — Choose from FIFO, LIFO, or HIFO

Zone B: Rules Banner

Section titled “Zone B: Rules Banner”For Australia, the rules banner is simpler than Canada or the US:

- No wash sale rule — Australia does not have an automatic loss denial rule

- No per-account tracking — No equivalent to the US T.D. 10000 requirement

- The banner shows the CGT discount status and your selected lot method

Zone C: Asset Table

Section titled “Zone C: Asset Table”After running a calculation, the asset table shows each cryptocurrency with:

- Total capital gain or loss

- Number of disposals

- CGT discount eligibility per disposal

- Calculation status and timestamp

Click any asset row to view the detailed CGT Worksheet for that asset.

Zone D: Calculation History

Section titled “Zone D: Calculation History”Shows all previous calculations with their parameters (method, tax year, timestamp) so you can compare results across different methods.

Running Your First AU Calculation

Section titled “Running Your First AU Calculation”- Import your transactions — Use CSV import with your exchange data. PrivateACB supports any exchange that provides transaction history.

- Select Australia — Click the jurisdiction toggle and choose Australia.

- Select your financial year — Choose the year (e.g., “2024-25”).

- Choose your method — FIFO is recommended if you’re unsure.

- Click Calculate — PrivateACB processes all transactions, creates parcels, matches disposals, and calculates gains/losses.

- Review results — Check the Asset Table for a summary. Click into individual assets for the full CGT Worksheet.

- Generate reports — Navigate to the Reports tab for your CGT Summary (Q18), CGT Worksheet, and other reports.

The 50% CGT Discount

Section titled “The 50% CGT Discount”This is the most significant AU-specific feature. If you are an Australian individual and you hold a CGT asset for more than 12 calendar months before disposing of it, you receive a 50% discount on the capital gain from that disposal.

Key Rules

Section titled “Key Rules”- Calendar months, not days: The check uses calendar months. An asset acquired on 15 January 2024 is NOT eligible until 16 January 2025. Exactly 12 months is not enough — you must exceed 12 months.

- Per-parcel basis: When a single disposal consumes multiple parcels, each parcel is checked independently. One parcel may be discount-eligible while another is not.

- Applied after netting losses: Capital losses are applied against gains before the discount is calculated (see Q18 Netting below).

- Individuals only: The 50% discount applies to individual taxpayers. Companies, super funds, and trusts have different rules.

Q18 Netting Algorithm

Section titled “Q18 Netting Algorithm”The ATO’s Question 18 on the Individual Tax Return uses a specific netting order:

- Add up all capital gains (separately tracking discount-eligible and non-eligible gains)

- Add up all capital losses

- Apply losses to non-discount gains first — this preserves the discount on eligible gains

- Apply remaining losses to discount-eligible gains — only if non-discount gains are exhausted

- Apply the 50% discount to remaining discount-eligible gains

- Net capital gain = remaining non-discount gains + discounted eligible gains

PrivateACB’s CGT Summary report shows this full netting worksheet, matching the ATO’s Q18 format.

What Australia Doesn’t Have

Section titled “What Australia Doesn’t Have”No Wash Sale Rule

Section titled “No Wash Sale Rule”Unlike the US, where selling at a loss and rebuying within 30 days can trigger a wash sale disallowance, Australia has no equivalent mechanical rule. You can sell crypto at a loss and immediately repurchase it without any automatic loss denial.

No Superficial Loss Rule

Section titled “No Superficial Loss Rule”Unlike Canada, where the CRA denies losses if you reacquire the same property within 30 days and still hold it 30 days later, Australia has no equivalent.

No Per-Account Tracking Requirement

Section titled “No Per-Account Tracking Requirement”Unlike the US T.D. 10000 requirement (effective 2025) to track cost basis per wallet/exchange, Australia does not require per-account tracking. All your parcels of the same asset are treated as a single pool for method selection purposes, regardless of which exchange or wallet they are held in.

Part IVA Anti-Avoidance

Section titled “Part IVA Anti-Avoidance”The only relevant anti-avoidance provision is Part IVA of the ITAA 1936, which is a general anti-avoidance rule. The ATO must demonstrate that a scheme was carried out with the dominant purpose of gaining a tax benefit. This is not a mechanical rule — it requires ATO audit and assessment. PrivateACB does not enforce Part IVA because it is intent-based, not formula-based.

Common Scenarios

Section titled “Common Scenarios”Short-Term Disposal (No Discount)

Section titled “Short-Term Disposal (No Discount)”You buy 1 ETH on 1 March 2025 for A$5,000 and sell on 1 August 2025 for A$7,000. Holding period: 5 months (less than 12 months). No CGT discount. Capital gain: A$2,000, fully assessable.

Long-Term Disposal (With Discount)

Section titled “Long-Term Disposal (With Discount)”You buy 1 ETH on 1 January 2024 for A$3,000 and sell on 15 February 2025 for A$5,000. Holding period: over 13 months. 50% CGT discount applies. Capital gain: A$2,000. After discount: A$1,000 included in assessable income.

Mixed Parcels in a Single Sale

Section titled “Mixed Parcels in a Single Sale”You sell 2 ETH, matched against:

- Parcel A (1 ETH, acquired 14 months ago): Gain A$1,500 — discount eligible

- Parcel B (1 ETH, acquired 3 months ago): Gain A$800 — no discount

PrivateACB calculates each parcel independently. After the Q18 netting algorithm, Parcel A’s gain is discounted by 50% while Parcel B’s is not.

Loss With No Denial

Section titled “Loss With No Denial”You buy 1 BTC for A$60,000 and sell for A$50,000 (loss of A$10,000). You immediately rebuy 1 BTC at A$50,000. In Australia, this is perfectly fine — the A$10,000 loss is fully available to offset against other capital gains. No 30-day waiting period, no denial, no adjustment.

Tax Year: July 1 to June 30

Section titled “Tax Year: July 1 to June 30”Australia’s financial year is different from the calendar year used by Canada and the US:

- “2024-25” means July 1, 2024 to June 30, 2025

- A BTC sale on March 15, 2025 falls in the 2024-25 financial year

- A BTC sale on August 1, 2025 falls in the 2025-26 financial year

PrivateACB displays tax years in the “2024-25” format throughout the app and correctly assigns all transactions to the right financial year based on the disposal date.

ATO Regulatory References

Section titled “ATO Regulatory References”- ITAA 1997, Section 104-10 — CGT event A1 (disposal of a CGT asset)

- ITAA 1997, Division 115 — CGT discount provisions

- ITAA 1997, Section 115-25 — 12-month ownership requirement for CGT discount

- ITAA 1997, Section 118-10 — Personal use asset exemption (< A$10,000 cost base)

- ATO Tax Determination TD 2014/26 — Bitcoin is a CGT asset, not foreign currency

- ATO Crypto Asset Guidance — Comprehensive guidance on CGT treatment

- ITAA 1936, Part IVA — General anti-avoidance provisions

- Guide: Capital gains tax (CGT) — ATO’s primary CGT resource